pandas-datareader一些用法备忘

pandas-datareader介绍

Pandas库提供了专门从财经网站获取金融数据的API接口,可作为量化交易股票数据获取的另一种途径

DataReader方法介绍

查看Pandas的操作文档可以发现,第一个参数为股票代码,苹果公司的代码为”AAPL”,国内股市采用的输入方式“股票代码”+“对应股市”,上证股票在股票代码后面加上“.SS”,深圳股票在股票代码后面加上“.SZ”。DataReader可从多个金融网站获取到股票数据,如“Yahoo! Finance” 、“Google Finance”等,这里以Yahoo为例。第三、四个参数为股票数据的起始时间断。返回的数据格式为DataFrame。

1

2

3

4

5

6

7

8

9

10

11

12

13

14

| import pandas as pd

from pandas_datareader import data

start_date = "2018-04-01"

end_date = "2021-04-01"

stock = data.DataReader(

"000001.SS", "yahoo", start_date, end_date

)

print(stock.head(5))

print(stock.tail(5), "\n")

print(stock.index)

print(stock.columns)

print(stock.shape)

|

结果:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

| High Low Open Close Volume Adj Close

Date

2018-04-02 3192.340088 3159.986084 3169.779053 3163.178955 177700 3163.178955

2018-04-03 3144.332031 3119.132080 3130.012939 3136.633057 152200 3136.633057

2018-04-04 3163.340088 3128.866943 3147.049072 3131.111084 147000 3131.111084

2018-04-09 3146.093018 3110.302979 3125.441895 3138.293945 139600 3138.293945

2018-04-10 3190.648926 3139.081055 3144.257080 3190.322021 168200 3190.322021

High Low Open Close Volume Adj Close

Date

2021-03-26 3423.222900 3373.316895 3373.316895 3418.326904 274600 3418.326904

2021-03-29 3449.833984 3409.886963 3429.632080 3435.300049 284800 3435.300049

2021-03-30 3457.629883 3423.320068 3432.530029 3456.679932 285400 3456.679932

2021-03-31 3452.209961 3420.830078 3452.209961 3441.909912 283000 3441.909912

2021-04-01 3470.030029 3438.830078 3444.810059 3466.330078 275200 3466.330078

DatetimeIndex(['2018-04-02', '2018-04-03', '2018-04-04', '2018-04-09',

'2018-04-10', '2018-04-11', '2018-04-12', '2018-04-13',

'2018-04-16', '2018-04-17',

...

'2021-03-19', '2021-03-22', '2021-03-23', '2021-03-24',

'2021-03-25', '2021-03-26', '2021-03-29', '2021-03-30',

'2021-03-31', '2021-04-01'],

dtype='datetime64[ns]', name='Date', length=728, freq=None)

Index(['High', 'Low', 'Open', 'Close', 'Volume', 'Adj Close'], dtype='object')

(728, 6)

|

数据分析

1、打印DataFrame数据前5行和尾部倒数5行

2、打印DataFrame数据索引和列名,索引为时间序列,列信息为开盘价、最高价、最低价、收盘价、复权收盘价、成交量

print stock.index

print stock.columns

3、打印DataFrame数据形状

print(stock.shape)

4、DataFrame数据每组的统计情况,如最小值、最大值、均值、标准差等

print stock.describe()

5、DataFrame数据中增加涨/跌幅列,涨/跌=(当日Close-上一日Close)/上一日Close*100%

(1)添加一列change,存储当日股票价格与前一日收盘价格相比的涨跌数值,即当日Close价格与上一日Close的差值,4月1日这天无上一日数据,因此出现缺失

1

2

3

4

5

6

7

8

9

10

11

12

13

14

| change = stock.Close.diff()

stock['Change'] = change

print(stock.head(5))

'''

High Low Open Close Volume Adj Close Change

Date

2020-04-01 2773.364014 2731.079102 2743.541016 2734.521973 217300 2734.521973 NaN

2020-04-02 2780.637939 2719.904053 2720.228027 2780.637939 217900 2780.637939 46.115967

2020-04-03 2780.586914 2754.072998 2773.575928 2763.987061 200800 2763.987061 -16.650879

2020-04-07 2823.277100 2801.839111 2806.968018 2820.762939 270200 2820.762939 56.775879

2020-04-08 2823.214111 2800.295898 2805.916992 2815.368896 243500 2815.368896 -5.394043

'''

|

(2)对缺失的数据用涨跌值的均值就地替代NaN。

change.fillna(change.mean(),inplace=True)

(3)计算涨跌幅度有两种方法,pct_change()算法的思想即是第二项开始向前做减法后再除以第一项,计算得到涨跌幅序列。

stock[‘pct_change’] = (stock[‘Change’] /stock[‘Close’].shift(1))#

stock[‘pct_change1’] = stock.Close.pct_change()

1

2

3

4

5

6

7

| High Low Open Close Volume Adj Close Change pct_change pct_change1

Date

2020-04-01 2773.364014 2731.079102 2743.541016 2734.521973 217300 2734.521973 NaN NaN NaN

2020-04-02 2780.637939 2719.904053 2720.228027 2780.637939 217900 2780.637939 46.115967 0.016864 0.016864

2020-04-03 2780.586914 2754.072998 2773.575928 2763.987061 200800 2763.987061 -16.650879 -0.005988 -0.005988

2020-04-07 2823.277100 2801.839111 2806.968018 2820.762939 270200 2820.762939 56.775879 0.020541 0.020541

2020-04-08 2823.214111 2800.295898 2805.916992 2815.368896 243500 2815.368896 -5.394043 -0.001912 -0.001912

|

7、DataFrame数据中增加跳空缺口数值序列,这里定义的缺口为上涨趋势和下跌趋势中的突破缺口,上涨趋势中今天的最低价高于昨天收盘价为向上跳空,下跌趋势中昨天收盘价高于今天最高价为向下跳空。遍历每个交易日后将符合跳空缺口条件的交易日增加缺口数值。

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

| import pandas as pd

from pandas_datareader import data

import numpy as np

start_date = "2020-04-01"

end_date = "2021-04-01"

stock = data.DataReader("000001.SS", "yahoo", start_date, end_date)

change = stock.Close.diff()

change.fillna(change.mean(), inplace=True)

stock["Change"] = change

stock["pct_change"] = stock["Change"] / stock["Close"].shift(1)

stock["pct_change1"] = stock.Close.pct_change()

jump_pd = pd.DataFrame()

for kl_index in np.arange(1, stock.shape[0]):

today = stock.iloc[kl_index]

yesday = stock.iloc[kl_index - 1]

today["preCloae"] = yesday.Close

if today["pct_change"] > 0 and (today.Low - today["preCloae"]) > 0:

today["jump_power"] = today.Low - today["preCloae"]

elif today["pct_change"] < 0 and (today.High - today["preCloae"]) < 0:

today["jump_power"] = today.High - today["preCloae"]

jump_pd = jump_pd.append(today)

stock["jump_power"] = jump_pd["jump_power"]

print(stock.loc["2020-04-01":"2021-04-01"])

|

结果:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

| High Low Open Close Volume Adj Close Change pct_change pct_change1 jump_power

Date

2020-04-01 2773.364014 2731.079102 2743.541016 2734.521973 217300 2734.521973 3.011556 NaN NaN NaN

2020-04-02 2780.637939 2719.904053 2720.228027 2780.637939 217900 2780.637939 46.115967 0.016864 0.016864 NaN

2020-04-03 2780.586914 2754.072998 2773.575928 2763.987061 200800 2763.987061 -16.650879 -0.005988 -0.005988 -0.051025

2020-04-07 2823.277100 2801.839111 2806.968018 2820.762939 270200 2820.762939 56.775879 0.020541 0.020541 37.852051

2020-04-08 2823.214111 2800.295898 2805.916992 2815.368896 243500 2815.368896 -5.394043 -0.001912 -0.001912 NaN

... ... ... ... ... ... ... ... ... ... ...

2021-03-26 3423.222900 3373.316895 3373.316895 3418.326904 274600 3418.326904 54.736816 0.016273 0.016273 9.726807

2021-03-29 3449.833984 3409.886963 3429.632080 3435.300049 284800 3435.300049 16.973145 0.004965 0.004965 NaN

2021-03-30 3457.629883 3423.320068 3432.530029 3456.679932 285400 3456.679932 21.379883 0.006224 0.006224 NaN

2021-03-31 3452.209961 3420.830078 3452.209961 3441.909912 283000 3441.909912 -14.770020 -0.004273 -0.004273 -4.469971

2021-04-01 3470.030029 3438.830078 3444.810059 3466.330078 275200 3466.330078 24.420166 0.007095 0.007095 NaN

[244 rows x 10 columns]

|

8、DataFrame数据保留两位小数显示

format = lambda x: ‘%.2f’ % x

stock = stock.applymap(format)

print stock.loc[“2017-04-26”:”2017-06-15”]#默认打印全部列

股价数据的可视化

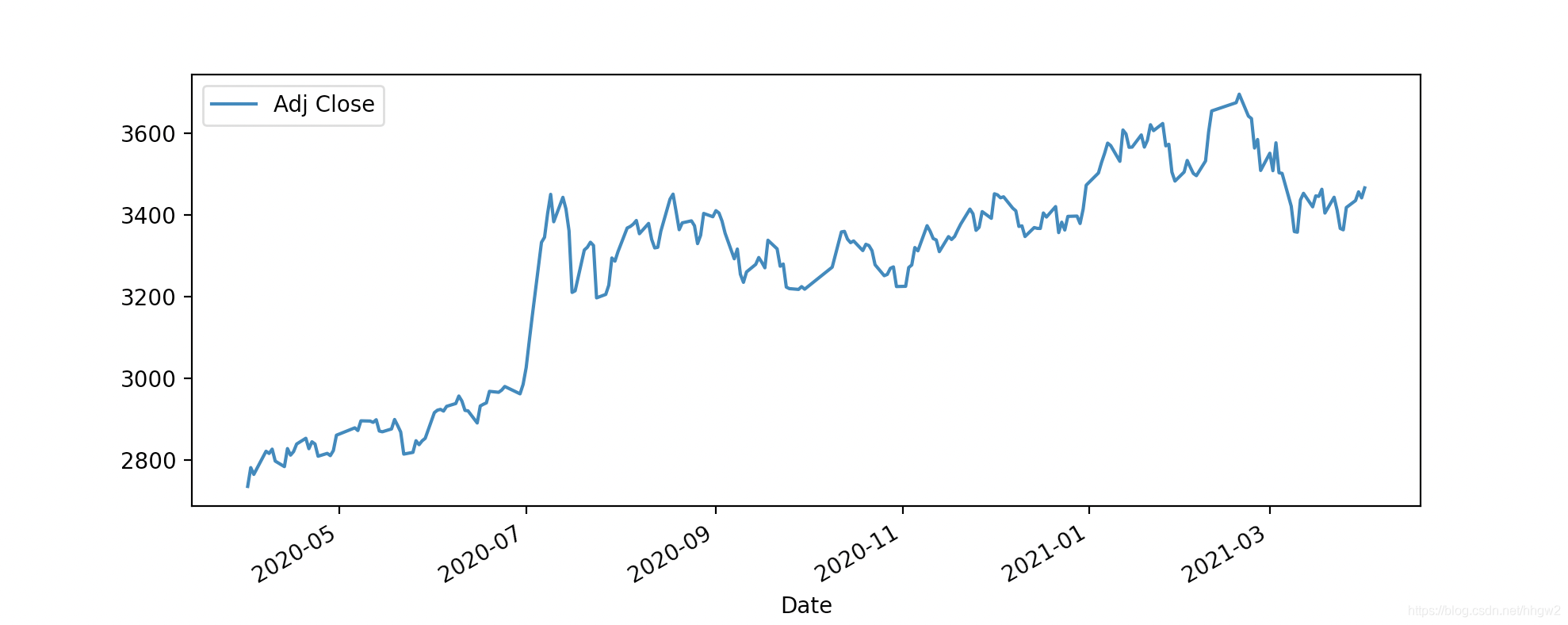

Matplotlib是使用Python进行绘图里非常方便的库。这次 plot使用的数据是 Adj Close栏的数据。这是所说的已调整收盘价。

如下仅仅需要两行写就可以简单的将股价作为时间序列数据画出来。

1

2

3

4

5

6

7

8

9

10

11

12

| import pandas as pd

from pandas_datareader import data

import numpy as np

import matplotlib.pyplot as plt

start_date = "2020-04-01"

end_date = "2021-04-01"

stock = data.DataReader("000001.SS", "yahoo", start_date, end_date)

stock['Adj Close'].plot(legend=True, figsize=(10,4))

plt.show()

|

实例操作:Python提取雅虎财经数据,并做数据分析和可视化

以csv格式存放

1

2

3

4

5

6

7

8

| import numpy as np

import pandas as pd

import pandas_datareader.data as web

import datetime

df_csvsave = web.DataReader("000001.SS","yahoo",datetime.datetime(2019,1,1),datetime.date.today())

print (df_csvsave)

df_csvsave.to_csv(r'C:\Users\15461\Desktop\table.csv',columns=df_csvsave.columns,index=True)

|

Author:

hhgw

License:

Copyright (c) 2023 CC-BY-NC-4.0 LICENSE

Slogan:

There is no fate but what we make.